On July l0, 1832, President Andrew Jackson sent a message to the United States Senate. He returned unsigned, with his objections, a bill that extended the charter of the Second Bank of the United States, due to expire in 1836, for another fifteen years. As Jackson drily noted, the bill was presented to him on the Fourth of July, a day freighted with portent.

Today Jackson's Bank Veto and the political conflagration known as the “Bank War” that it touched off seem arcane and nearly incomprehensible. While misdeeds among the rich and powerful still garner headlines and incite congressional inquiries, the core instruments of our economic system-the network of banks capped by the Federal Reserve; the corporate form of business enterprise; the very dollars in our wallets, issued and guaranteed by the federal government—are utterly taken for granted. That these could have been the subject of controversy, that anyone could seriously contemplate organizing American capitalism differently, seems nearly unthinkable. Andrew Jackson is recalled today, when recalled at all, for other things, primarily as the architect of forced Indian removal. His face on the $20 bill is a mystery to many, an outrage to some, and, to the knowing, a curious irony.

Yet, in its day, nothing galvanized American political conflict more than banking, currency, and finance. In the republic's first half-century, no subject, save foreign relations and war, gave greater vexation to American statesmen or aroused more heated public debate. The creation of the original Bank of the United States in 1791 sparked the first major division within President George Washington's administration, which later ripened into the Federalist and Democratic-Republican parties. Jackson's veto in 1832 repeated the process: It became the touchstone issue in his reelection campaign and precipitated the organization of the Whig and Democratic parties, the latter, still surviving, now the oldest mass political party in the world. The very language of Jackson's veto, departing sharply from all that came before, furnished a political grammar since claimed by Populists, Progressives, New Deal liberals, socialists, free marketeers, libertarians—in short, by just about everybody.

Clearly, one cannot fully appreciate Jacksonian, and indeed American, politics without confronting his Bank Veto. Yet to make sense of the document requires imagining a world in some ways very different from our own. Americans were already by the time of the Revolution a famously enterprising people, yet their enterprise required capital far beyond available means. Credit was vital but often uncertain. The country's only legal money, gold and silver coin, was in chronic shortage, never plentiful enough to serve in everyday exchange. Banking in the early United States therefore grew by the forced hand of government. By special individualized acts of legislation, state and federal governments incorporated banks and authorized them to lend their own credit in the form of banknotes. Ostensibly redeemable in specie, these notes passed in lieu of coin in daily commerce, serving in practice, though not in law, as money.

The connection of banks and government was fraught with financial and political peril, especially in a young republic whose citizens craved riches and yet resented every hint of aristocratic privilege. Banking was poorly understood, not yet professionalized, and its amateur practitioners sometimes wreaked disaster on their customers. Indeed, men commonly sought bank charters not as an outlet for investment, but as a source of credit—not looking to lend, but to borrow. In a financial sleight of hand, the required paid-in capital to start a bank often consisted of IOUs to be redeemed by the bank's own profits.

That lawmakers could ordain credit, and hence create wealth, by merely waving a legislative wand struck many citizens as strange and malign. Corporations themselves were a novel form of business organization, not yet standardized or widely utilized. To many simple farmers and tradesmen, the granting of special favors, including the prize of limited liability, by means of legislative bank charters recalled the hated British system of monopoly and corruption. Paper money was also suspect-with good reason, since if issued imprudently it had a way of becoming worthless. No less than former President John Adams in 1813 damned chartered banking as a giant swindle, a "Sacrifice of public and private Interest to a few Aristocratical Friends and Favourites."

In 1790, Treasury Secretary Alexander Hamilton proposed to incorporate a Bank of the United States. Modeled on the Bank of England, it was intended frankly to buttress the new government by entangling its finances with the interests of moneyed men. Though serving public purposes, the Bank was to be a profit-making institution, with private shareholders holding four-fifths of its stock and electing four-fifths of its directors. It was, said Hamilton, “an essential ingredient” in inspiring confidence in its prudent management that a national bank "be under a private not a public direction, under the guidance of individual interest, not of public policy."

Opposed by Secretary of State Thomas Jefferson and his ally James Madison, Hamilton's Bank nonetheless passed Congress and became law. In operation it accomplished all its architects had hoped, stabilizing the country's chaotic currency and helping retire its Revolutionary debt. But many Jeffersonians never accepted it, and when its twenty-year charter came up for renewal in 1811, with Congress in their control, they killed it.

The government's ensuing flirtation with bankruptcy in the War of 1812 taught them their mistake. In 1816, Congress chartered a Second Bank, again for twenty years. Like its predecessor, it was a predominantly private entity serving public purposes. The four-to-one private-public ratio in ownership and directorate was retained, and the Bank's capital was advanced from $10 to $35 million, a huge sum in those days. Authorized to establish branches throughout the states, the Bank was the country's only financial institution of truly national reach. While competing with state-chartered banks for private business (and controlling their lending by collecting their notes for redemption), it would also be the federal government's banker, charged with brokering its loans and with receiving, storing, transporting, and disbursing federal funds. The Bank's notes were legal tender. In return for its “exclusive privileges and benefits,” including a congressional pledge to create no competing institution, the Bank was to pay the government a bonus of $1.5 million.

Opening for business in the midst of a postwar boom, the Second Bank promptly discredited itself by speculation, stockjobbing, and, at some branches, outright fraud. But under the discreet management of its second president, Langdon Cheves, and his successor, Nicholas Biddle, it soon repaired its condition and reputation. By the end of the 1820s it had proved not only useful but, to many eyes, indispensable.

But not to Andrew Jackson. Jackson came to the presidency with a deep sense of grievance against his enemies, real and imagined, in the existing political establishment and with a conviction that the government had fallen from Jeffersonian austerity into profligacy and corruption. This he was determined to reverse. The Bank was barely mentioned in Jackson's 1828 successful campaign against incumbent John Quincy Adams. But, after assuming office, Jackson learned of branch officers using the Bank as what one Jackson partisan called “an engine of political oppression” against his followers. Asked to explain, Bank president Biddle pronounced the charges “entirely groundless.” He affirmed the Bank's forbearance from politics-and its complete independence from executive control.

Then, in November 1829, Biddle approached Jackson with a proposition. The Bank would assume the last of the dwindling national debt to enable its full discharge before the end of Jackson's term, an object that Biddle knew was dear to the president's heart. The quid for this quo was an early recharter for the Bank, which would send its stock soaring and provide a windfall for shareholders.

Intended to placate Jackson by showing the Bank's friendship and usefulness, Biddle's offer had the opposite effect. To Jackson it was a backstairs deal smelling of privilege and corruption, something close to a bribe. Already suspicious of the Bank, from that moment he turned irrevocably against it. In his first annual message to Congress just a few weeks later, he startled everyone by raising the question of recharter and declaring his opposition. The Bank's constitutionality and expediency were “well questioned,” said Jackson, “and it must be admitted by all that it has failed in the great end of establishing a uniform and sound currency.” It was a statement at variance with facts. The Bank's notes, unlike those of many state-chartered banks, circulated everywhere at face value, their integrity unquestioned. They were as good as gold.

To Jackson it did not matter. In the Bank, Jackson found a concrete focus for all his fears of aristocratic subversion—fears he shared with many citizens. “I was aware that the Bank question would be disapproved by all the sordid, & interested, who prised self interest more than the perpetuity of our liberty, & the blessings of a free republican government,” he confided shortly after the annual message. “This monied aristocracy” was everywhere at work, buying up voters and lawmakers and “silencing opposition, by its corrupting influence, & preparing for a renewal of its charter, which I viewed as the death blow to our liberty.”

The recipient of this disclosure was none other than James Alexander Hamilton, son of the late Treasury secretary and himself a federal district attorney and Jackson confidant. Hamilton had helped craft the passage opposing recharter in the annual message. Now, at Jackson's prompting, he prepared a detailed critique, arraying objections to the Bank under two heads. The Bank was unconstitutional, because Congress had no power to charter corporations and withdraw them from the regulatory and taxing power of the states. (This was the Jeffersonian position, which the Supreme Court under Chief Justice John Marshall had rejected in the landmark case of McCulloch v. Maryland in 1819.) The Bank was also dangerous to liberty, because its concentrated power gave it a “fearful influence” over citizens' lives and an unchecked sway over government, inviting corruption and oppression.

Jackson copied Hamilton's headings into his private memorandum book. Over the next two years, he recopied and reworked his bill of particulars, always under the same two heads: The Bank was unconstitutional, and it was dangerous to liberty. Meanwhile, the question of recharter simmered. In his 1830 and 1831 annual messages, Jackson reiterated his opposition to the Bank. He proposed in its stead a wholly government institution—in name a bank, but in effect an arm of the Treasury, without power to make loans, acquire property, or issue notes.

In 1832, Congress acted, but not as Jackson recommended. A bill to extend the charter, slightly modified, of the existing Bank passed both houses by healthy majorities, though less than the two-thirds required to override a veto. To Jackson the bill's timing confirmed his strictures about the Bank's meddling in politics. Biddle had decided to press for recharter at the urging of Senator Henry Clay, Jackson's opponent in the presidential election only months away. In effect, they dared Jackson to veto.

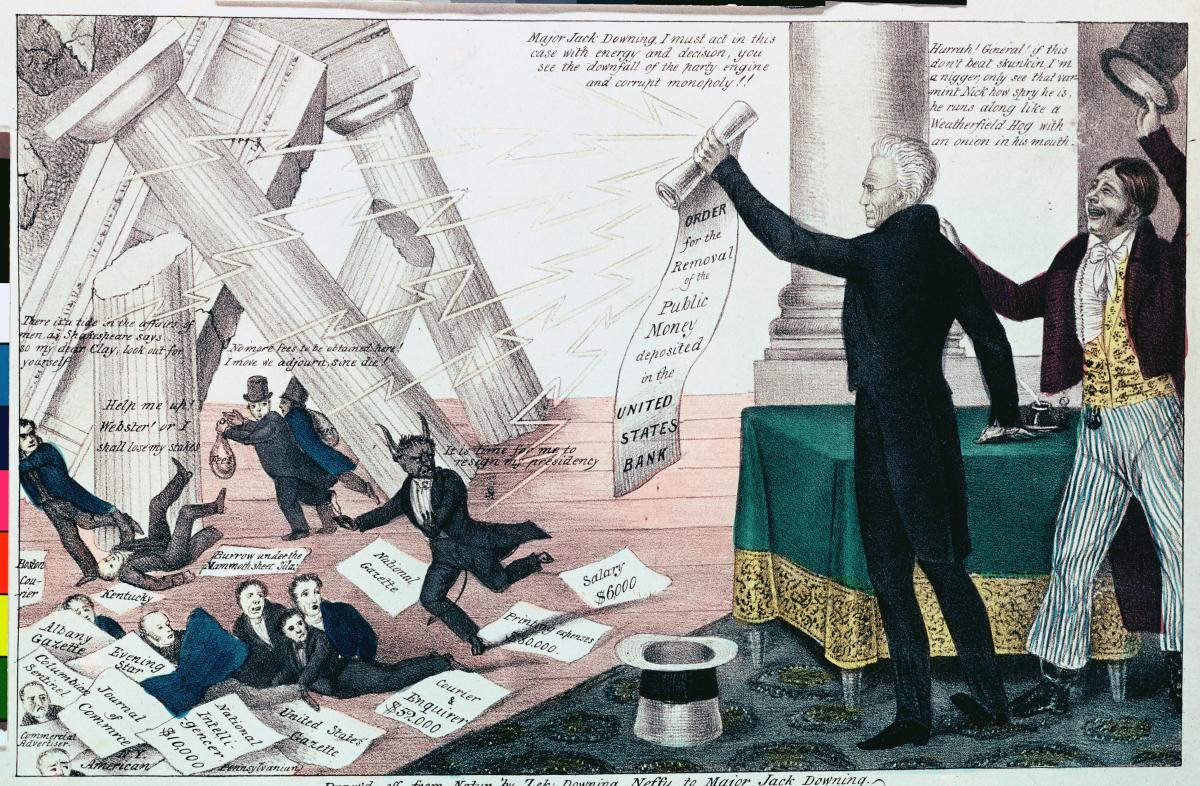

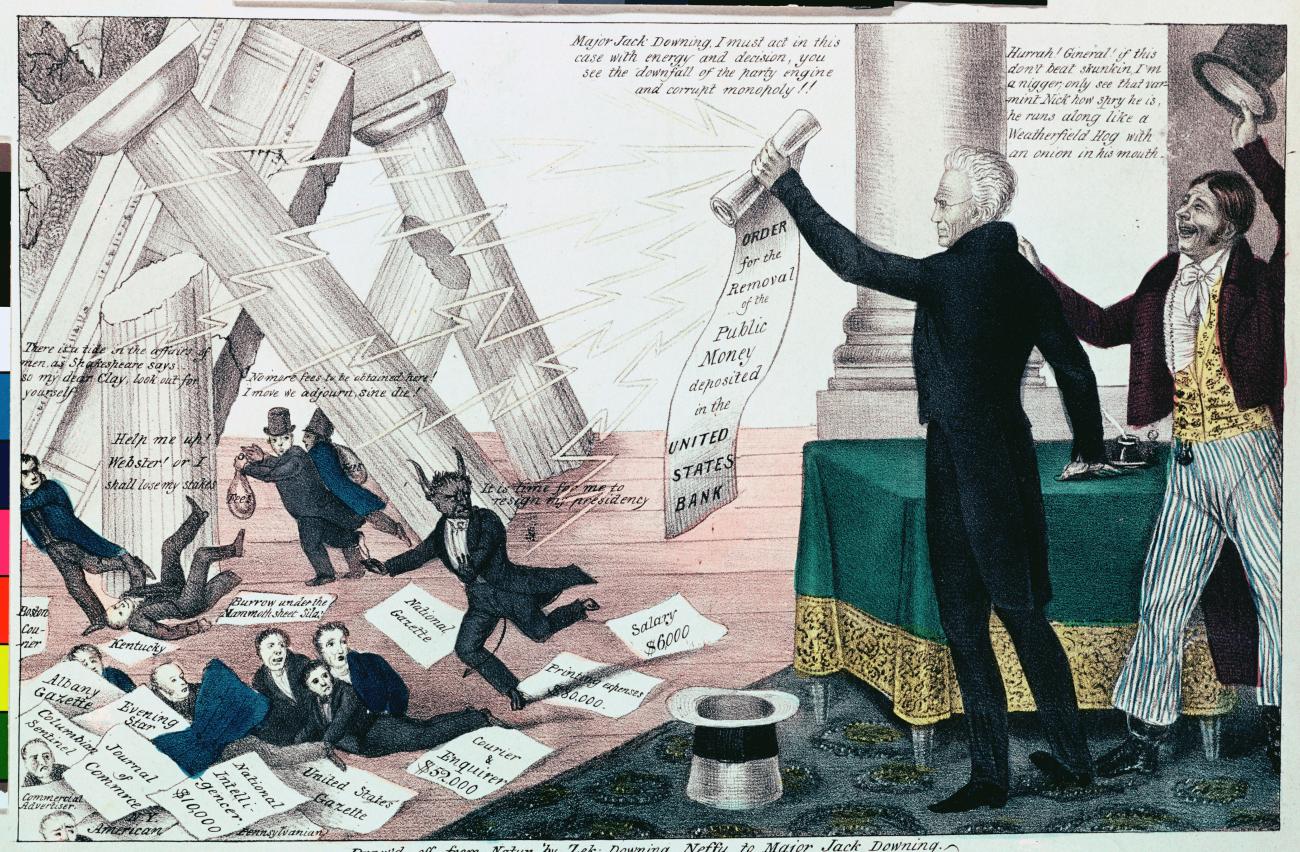

"Downfall of Mother Bank" by Henry R. Robinson, 1833.

© Collection of the New York Historical Society / Bridgeman Art Library

"Downfall of Mother Bank" by Henry R. Robinson, 1833.

© Collection of the New York Historical Society / Bridgeman Art Library

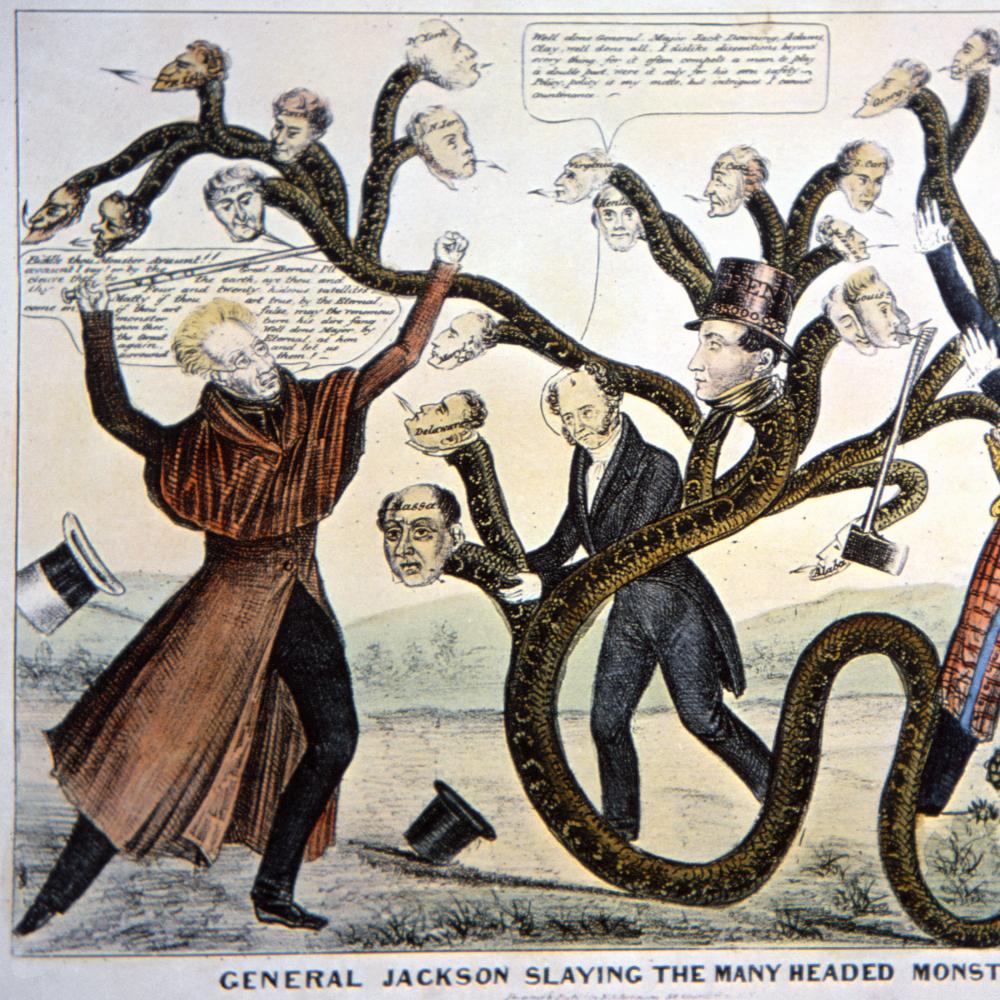

He did, in a message that became the rhetorical apex of his presidency. Treasury official Amos Kendall and other wordsmiths helped hone the Veto, but the governing ideas, drawn straight from Jackson's memoranda, were clearly his own. Following Jefferson, and contradicting the Supreme Court in McCulloch, Jackson denied the Bank's constitutionality and affirmed his right to judge that question independent of Congress or the courts. Ingeniously, and perversely, he targeted foreign stockholders for special censure. Much of the Bank's stock was, in fact, held abroad, especially in Britain. The charter screened management from foreign interference by barring noncitizens from serving as directors or voting their shares. They could invest, but not control. By an economist's rationale, a more benign vehicle for inviting capital into America's developing economy could hardly be contrived. Yet Jackson's arguments turned investment into subversion. Bank dividends, he complained, siphoned off American money overseas, and the immunity of foreign stockholders from domestic taxation would lure ever more stock abroad, concentrating the Bank's control within a narrowing sphere of domestic holders and inviting their subservience to foreign dictation. “If we must have a bank,” Jackson warned, “it should be purely American.”

But the real heart of the Veto was its attack on exclusivity and favoritism. Sounding the loaded words “monopoly” and “privilege” over and over like a tocsin, Jackson laid out his core theme: The Bank's charter gave its stockholders a promise of pelf and power not accessible to other citizens. It made them “a privileged order, clothed both with great political power and enjoying immense pecuniary advantages from their connection with the Government.” Jackson's peroration conveyed both the Veto's essential meaning and its inescapable ambiguity:

It is to be regretted that the rich and powerful too often bend the acts of government to their selfish purposes. Distinctions in society will always exist under every just government. Equality of talents, of education, or of wealth can not be produced by human institutions. In the full enjoyment of the gifts of Heaven and the fruits of superior industry, economy, and virtue, every man is equally entitled to protection by law; but when the laws undertake to add to these natural and just advantages artificial distinctions, to grant titles, gratuities, and exclusive privileges, to make the rich richer and the potent more powerful, the humble members of society-the farmers, mechanics, and laborers-who have neither the time nor the means of securing like favors to themselves, have a right to complain of the injustice of their Government. There are no necessary evils in government. Its evils exist only in its abuses. If it would confine itself to equal protection, and as Heaven does its rains, shower its favors alike on the high and the low, the rich and the poor, it would be an unqualified blessing.

In all the presidential messages—inaugurals, annuals, vetoes—that came before, there is nothing like this. Other presidents had sometimes warned Americans of foreign perils, or the dangers of factionalism and divisiveness among equally well-disposed and meritorious citizens. Andrew Jackson warned them against their government—and each other.

And yet, what exactly does it mean? Jackson's frank branding of Americans by occupation and circumstance, his bold counterposing of rich and poor, and his solicitude for the working “farmers, mechanics, and laborers” against the “rich and powerful” seemed to many then and later a promulgation of class warfare—an anathema to some, a battle cry for others. Yet his acknowledgment of inevitable wealth disparities and his solution of “equal protection” and minimalist government echo more of market economics than of the welfare state. Some historians see Jackson in a straight line of working-class champions, foes of capitalist dominion, running from Thomas Jefferson through Franklin Roosevelt. Others see him as the spokesman of enterprise, assailing a confining, repressive politico-economic establishment to liberate the wealth-creating energies of “superior industry, economy, and virtue.” There is strong evidence on both sides.

And still another question lurks. If Jackson pointedly stretched the ranks of people who mattered politically to include “farmers, mechanics, and laborers,” did that portend a further extension, beyond the white male electorate, to include women, slaves, and Indians? Without question, Jackson did not himself intend so. But words once spoken may have a life of their own. Whether one sees Jackson's invocation of “the humble members of society” as weighing on the side of inclusion or exclusion, erecting boundaries or breaking them down, has everything to do with how one judges his legacy and reputation.

The veto held up in Congress, as all knew it would. In the ensuing campaign, both sides, remarkably, distributed the message as a campaign document-Jacksonians to show his patriotism and egalitarianism, foes to exhibit his ignorance and demagoguery. Jackson trounced Clay in the election. Afterwards, to defang the Bank, whose present charter was still in effect and whose political resourcefulness was by no means exhausted, Jackson withdrew the federal government's deposits and lodged them with various state-chartered banks. Biddle retaliated by curtailing loans, causing business distress. Intended to force a recharter, his action instead discredited the Bank by reinforcing Jackson's warnings of its irresponsible power. Jackson's removal of the deposits prompted his foes to coalesce under the name of Whigs, a term denoting opponents of royal prerogative. In 1834, a Whig Senate formally censured Jackson—an action which Jacksonians, now calling themselves Democrats, expunged from the Senate record as soon as they gained a majority. The defeated Bank accepted a charter from the Pennsylvania legislature and continued after 1836 as a state institution.

The destruction of the Bank loosed American enterprise from its only central restraint. Gorged with federal deposits and with no one to control their note issues, state banks went on a lending spree that built up a speculative bubble and ended, just as Jackson left office in 1837, in a sickening crash. Jackson's culpability for the ensuing depression is still debated. Jackson himself came to oppose all chartered banks and banknotes, state as well as federal, and to favor a return to gold and silver “hard money”—a radical deflation which Whigs charged would throw progress back a century. In Jackson's farewell address on retiring from office, he elaborated the language of the Veto, condemning bank paper as an engine of oppression and warning of the insidious "money power" and of the growing control exerted by faceless corporations over ordinary citizens' lives.

Jackson's Democratic successors Martin Van Buren and James K. Polk cemented his victory over the Bank. A new independent Treasury assumed the handling of government finances, realizing Jackson's aim of severing government from the business of banking. For a generation, that business remained semi-organized and essentially directionless. The exigencies of the Civil War forced the first steps toward nationalizing the banking system and the currency, a process completed with the creation of the Federal Reserve in 1913.

The immediate circumstances that prompted Andrew Jackson's ringing expostulations have long since passed away. Whether his words carry an enduring message would be for later generations, including our own, to decide for themselves.