Administration of NEH Challenge Infrastructure and Capacity Building Grants

For NEH Infrastructure and Capacity Building Challenge Grants with a federal award identification number prefix “CHA” issued from 2018 through January 31, 2022.

Published August 16, 2018 (Updated on January 30, 2025, to reflect changes to the dollar threshold for submitting individual donor documentation with the gift certification to NEH.)

NEH awards are subject to the National Foundation on the Arts and the Humanities Act of 1965 (P. L. 89-209, as amended; 20 USC §956 et seq.); 2 CFR Part 200 – Uniform Administrative Requirements[i], Cost Principles, and Audit Requirements for Federal Awards; the General Terms and Conditions for Awards to Organizations (for grants and cooperative agreements issued December 26, 2014 or later)[ii]; and the specific terms and conditions in the notice of award. Should there be any inconsistency between the specific terms and conditions of an award and the General Terms and Conditions for Awards, the specific terms and conditions will govern. Should there be any inconsistency between the General Terms and Conditions for Awards and the Administration of NEH Challenge Grants, the latter will govern.

In accepting an award, the recipient assumes the legal responsibility of administering the award in accordance with these requirements and of maintaining documentation, which is subject to audit, of all actions and expenditures affecting the award. Failure to comply with these requirements could result in suspension or termination of the award.

Recipients are encouraged to contact NEH staff via eGMS Reach[iii], NEH’s online grant management system.

TABLE OF CONTENTS

II. Release of Federal Funds (with sample release schedule)

III. Eligibility of Matching Gifts

- General Criteria

- Kinds of Eligible Gifts

- Pledges

- Planned Gifts

- Foundation Gifts

- Ineligible Gifts

- Record Keeping (with Sample Donor Transmittal Letter)

- Certification

- Additional Documentation

V. Payment

VI. Failure to Meet Required Match

- Forfeiture

- Refunds

- Extensions

- Annual Certifications

- Interim Performance Reports

- Final Performance Report and Certification

- Follow-up Reports

- Final Federal Financial Report (FFR) SF 425

- Extensions for Reports

VIII. Acknowledgment Guidelines

- Certification Form

- Special Requirements for Construction and Renovation Projects

- Federal Interest in Real Property

I. Basic Principles

- When matched by nonfederal donations and subject to the availability of funds, federal funds will be made available for payment according to the schedule described in the offer letter.

- To count toward the matching requirement, restricted gifts must be donated or pledged in anticipation of, in response to, or restricted by the donor to the same purpose as the NEH challenge grant.

- The total of unrestricted gifts that may be certified cannot exceed the amount of the federal portion of the challenge grant.

- To count toward the matching requirement, all gifts must be donated or pledged, and all pledges paid, during the approved fund raising period (five months prior to the application deadline through the end date of the period of performance). The period of performance, also known as the award period, is on your notice of award.

- All federal and nonfederal challenge grant funds must be expended during the period of performance. Funds earmarked for endowment (or spend-down funds) in the approved budget are considered to be "expended" upon deposit into an income-earning account established as a short-term endowment fund.

- Challenge grant funds, both federal and nonfederal, may be used only to support the purposes outlined in the approved challenge grant application. Where the grant supports more than one activity, donations restricted to any one activity are limited to the amounts indicated in the approved challenge grant budget.

- For challenge grants funding construction projects: overhead and indirect costs are unallowable. Contingency amounts must be used for actual costs incurred in compliance with 2 CFR 200 Subpart E – Cost Principles[iv]. Contingency costs may not include amounts for major project scope changes, unforeseen risks, or extraordinary events.

- Grant recipients are responsible for accurate internal record keeping, for timely certification of gifts, and for submission of required documentation and reports to NEH.

- Endowments created with NEH challenge grants are restricted to the uses defined in the challenge grant budget as approved.

II. Release of Federal Funds

All federal challenge grant funds are matching funds. The federal portion of a regular challenge grant with a three or four-to-one matching ratio and a five-year period of support is typically offered in four annual installments. NEH releases federal funds according to a pattern that allows donations as early as five months prior to the application deadline through the period of performance. For regular challenge grants, funds are released in the first three years when completely matched according to the required amount. The fourth year's installment allows the release of the federal funds when matched one-to-one, with the remaining parts of the match to be raised in the final year, to allow time in the final year of the period of performance to finish the match and collect outstanding pledges.

The following chart illustrates a typical match and release schedule.

NOTE: The following chart is only a sample. Each grant has a unique match and release schedule, as outlined in the challenge grant offer letter. Special initiative challenge grants, for example, have a longer period of performance than regular challenge grants.

Sample Match and Release Schedule

NEH Challenge offer of $300,000, with a three-to-one matching ratio

Year 1

Year 2

Year 3

Year 4

Year 5

Total

NEH funds (federal) offered

$25,000

$100,000

$100,000

$75,000

n/a

$300,000

Nonfederal funds to be raised

$75,000

$300,000

$300,000

$75,000

$150,000

$900,000

Total challenge funds

(federal + nonfederal)

$100,000

$400,000

$400,000

$150,000

$150,000

$1,200,000

The federal portion of challenge grants with a one-to-one matching ratio to Historically Black Colleges and Universities (HBCU), Tribal institutions of higher education, Hispanic serving institutions, and two-year colleges is typically released in six annual installments over a six-year period of performance. NEH releases funds when completely matched according to the required one-to-one ratio. The fundraising period begins as early as five months prior to the application deadline and can include donations through the period of performance

Sample match and release schedule for a challenge grant to an HBCU, a Tribal College or University, a Hispanic-serving institution of higher education, or a two-year community college

EXAMPLE ONLY: NEH Challenge offer of $300,000, with a one-to-one matching ratio

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Total

NEH funds

(federal) offered

$25,000

$75,000

$100,000

$50,000

$25,000

$25,000

$300,000

Nonfederal funds

to be raised

$25,000

$75,000

$100,000

$50,000

$25,000

$25,000

$300,000

Total challenge funds

(federal + nonfederal)

$50,000

$150,000

$200,000

$100,000

$50,000

$50,000

$600,000

Variations on a typical match and release schedule are possible, and recipients should discuss with NEH staff the schedule that most accurately reflects the institution's plans and fundraising capacity. NEH, however, makes the final determination of the match and release schedule.

Grant recipients are encouraged to certify gifts in advance of the required matching schedule. In some instances, depending on available program funds, advance certification may result in the early release of federal funds.

III. Eligibility of Matching Gifts

A. General Criteria

The following criteria govern the eligibility of matching gifts. Questions about the eligibility of a gift should be raised with Endowment staff prior to certification.

Restricted gifts must be in response to, in anticipation of, or restricted by the donor to the same purpose as the challenge grant. Except in the case of certain types of planned gifts (such as bequests), donors of restricted gifts must be aware that their gifts are to be used for the same purpose as described in the approved challenge grant application. Proof of donor awareness can be in the form of individual transmittal letters (required for restricted gifts of $25,000 or more—see Section IV.A for a sample letter). Other evidence of donor intent can be in the form of membership or alumni solicitation mailings; newsletters; public notices regarding contributions, admission fees, or gift shop sales; posters or other publicity for fundraising events; scripts for telethons or for radio or television solicitations; or other written documentation that can verify the donor's intent that the gift be used for the same purpose as the challenge grant.

Unrestricted gifts—gifts that may be used at the recipient's discretion and that have not been restricted to or designated for any specific purpose — may be certified only up to an amount equal to the federal portion of the challenge grant. Funds previously designated for any specific purpose may not be changed to unrestricted funds. Deposit of a gift into an unrestricted gift fund or a general operating fund is not considered to be “designated to a specific purpose,” and may be used for a challenge grant if the gift was given within the fundraising period (five months prior to the application deadline through the end date of the period of performance).

NOTE: Three categories of donations -- in-kind gifts, earned income, and unrestricted gifts -- are each limited in amount to the federal portion of the challenge grant. Furthermore, the total of these three categories of gifts, added together, may not exceed the federal portion of the challenge grant.

The matching gift must be used to support the purposes outlined in the approved challenge grant application. For example, if a college received a challenge grant for the purpose of renovating classrooms for humanities programs, and if a donor then contributed a piece of art to the school's museum for the purpose of sale, the contribution would not be eligible for matching unless converted to cash before the end of the period of performance.

All matching gifts, restricted and unrestricted, must be given and pledges paid during the fundraising period (five months prior to the application deadline through the end date of the period of performance). A pledge can be used to release federal funds as long as that pledge commitment is paid within the fundraising period and meets the other eligibility criteria. A pledge commitment made before the fundraising period begins cannot itself count toward match; payments in fulfillment of such a pledge can count if they meet the other eligibility requirements.

Gifts may not derive from the grant recipient institution itself. It is inappropriate for an institution to shift internal budgets, sell assets already owned, or reallocate internal funds for matching purposes. Unrestricted gifts of either assets or funds donated within the fundraising period (five months prior to the application deadline through the end date of the period of performance) can be reclassified as a challenge grant gift. At that point, the gift will be placed in the challenge grant account. Income from endowed funds is not new income, and recipients may not include as part of their match any interest earned on gifts made for challenge grant purposes. Gifts or grants from foundations may count toward the match except in the case of challenge grant recipient institution-specific foundations. An institution-specific foundation may not make donations to its own institution's challenge grant. Different kinds of foundations are treated differently for matching purposes. See Section III.E.

Normally challenge grant funds, both the federal and nonfederal portions, are received, held, and managed by the grantee institution. Any other arrangement (for example, with university foundations, friends groups, community foundations, parallel foundations, donor-advised funds) requires advance approval from NEH.

B. Kinds of Eligible Gifts. Grant recipients must account for the eligibility of all matching funds, and their records are subject to audit. Copies of transmittal letters and other documentation required for gifts must be submitted with the certification form. To be eligible as a restricted gift, the gift must represent a specific and documented response either to the NEH challenge or for the purposes of the grant. The following are the principal kinds of gifts that may be eligible as matching donations:

- Cash.

- Nonfederal grants.

- Special legislated nonfederal appropriations from state, county, or municipal governments. The appropriation must represent a level of support above the normal appropriation for the grantee institution. Legislated nonfederal appropriations may count only as restricted gifts, not as unrestricted gifts. To count as restricted gifts the legislative or budgetary language should make explicit reference to the NEH challenge grant, or to the purpose of the challenge grant.

- Net proceeds from special fundraising events or benefits held specifically to raise matching funds for an NEH challenge grant. Only the net proceeds are eligible; the intrinsic value of the items donated for auction or sale is not eligible.

- Membership contributions, "friends" or alumni giving, or similar campaigns. The value of any tangible items received by donors, such as magazines, newsletters, or gift "premiums," must be deducted from a membership contribution to assess the actual gift value. Membership forms or solicitation materials should be submitted to NEH and should indicate that contributions will be used for challenge grant matching purposes.

- Earned income, such as income from publication or gift shop sales. Only the net income is eligible. Earned income may count only as restricted gifts, not as unrestricted gifts. To count as restricted gifts, such sales must be clearly identified as responses to the challenge grant or to the purposes of the challenge grant. The total amount of earned income allowed may not exceed the federal portion of the challenge grant.

- Marketable securities, valued as of the date of transfer from donor to grant recipient.

- Real estate, if the property is converted into cash by means of sale. The value of the gift is equivalent to the net sale value. Real estate may also be eligible as an in-kind gift (see III.B.9. below) if the property is integral to the humanities activities supported by the challenge grant. Income produced by donated property (such as rent) may also be eligible for matching. Per 2 CFR §200.306[v] (d), the value of such an in-kind gift is equivalent to the lesser of the following:

- The value of the remaining life of the property recorded in the recipient’s accounting records at the time of the donation.

- The current fair market value.

(See "Additional Documentation," Section IV.C.)

9. In-kind gifts or donated services are eligible only if the material or service provided is appropriate to the approved purposes of the challenge grant and is approved in advance by NEH. Gifts of tangible property not appropriate to the approved purposes of the challenge grant must be converted to cash to qualify for match. In-kind donations may count only as restricted gifts, not as unrestricted gifts. The total amount of in-kind gifts or donated services allowed may not exceed the federal portion of the challenge grant. (See "Additional Documentation," Section IV.C.)

NOTE: Three categories of donations -- in-kind gifts, earned income, and unrestricted gifts -- are each limited in amount to the federal portion of the challenge grant. Furthermore, the total of these three categories of gifts, added together, may not exceed the federal portion of the challenge grant.

C. Pledges. Pledges may count toward the release of federal funds when made during the fundraising period (five months prior to the application deadline through the end date of the period of performance), but all pledges must be paid and expended before the end of the period of performance. Such pledges must be in writing and constitute a legally binding promise to pay (for a sample pledge letter, see Section IV.B.). Similarly, a nonfederal grant (gift category 2, above) may count toward matching when awarded during the fundraising period, but the pledge must be paid and expended before the end of the period of performance. Legislated appropriations (gift category 3, above) may count toward matching when passed by the appropriate legislative body during the fundraising period, but the appropriation must be paid and expended by the challenge grant recipient before the end of the period of performance. However, a contract for the sale of real estate (gift category 8, above) may not count toward the matching requirement prior to the final completed sale.

D. Planned Gifts. In order to qualify as a gift eligible for federal matching through the NEH Challenge Grants program, an instrument of planned giving must meet the following conditions:

- The value of the gift must be determinable and unchangeable.

- The gift must be irrevocable.

- The gift must be expendable within the period of performance for the purposes of the challenge grant.

- The gift must be given (or pledged) within the fundraising period (five months prior to the application deadline through the end date of the period of performance). All pledges must be paid and expended before the end of the period of performance.

Examples:

Charitable Gift Annuity (CGA): A CGA is a contract between the donor and the institution by which the donor makes a donation and the institution agrees to pay the donor a set amount each year until the donor's death. The Internal Revenue Service recognizes a portion of the donation as a charitable gift. This gift portion of the annuity received during the fundraising period (five months prior to the application deadline through the end date of the period of performance) may be eligible for matching. A copy of the annuity contract and a copy of the letter from the institution indicating the allowable tax deduction (including the calculations by which the tax deduction was determined) must accompany the certification form in which a CGA is included. If the annuity is intended as a restricted gift, a copy of the donor transmittal letter should also be sent to NEH. The gift portion of the CGA must be expended for the costs as shown in the approved Challenge Grant budget before the end of the period of performance.

Bequest: A "bequest intention," that is, a statement in a will that a donor is bequeathing a gift to the institution for the challenge grant is not itself certifiable for matching. The bequest must have been realized (that is, the donor must have died), so that the bequest can be paid by the estate. It is the date on which the estate pays the bequest to the grant recipient that determines its timeliness. The dollar amount of the bequest must be determined before it can be certified for match; a percentage bequest, a residual bequest, or a contingent bequest cannot be certified before the amount is determined. Once the value of a bequest is finally determined, it may be certified as a pledge or, if paid, as a cash payment. To qualify as a restricted gift, the will must refer to the challenge grant or to the humanities activities to be supported by the challenge grant. A bequest that does not refer to the challenge grant or to the challenge-grant supported activities, and that has not been designated by the donor or the grantee for some other purpose, may be matched as an unrestricted gift, up to the limit on total unrestricted gifts. A copy of the portion of the will containing the bequest intention must be submitted with the certification form in which the bequest is included. All bequest pledges used to certify the match must be paid and expended before the end of the period of performance

Gift from an estate: An estate may have the authority to designate a gift for the challenge grant. For such a gift, the grantee must submit to NEH a copy of the portion of the will establishing authority for estate-determined gifts.

Grant recipients should consult NEH staff before certifying these or any other types of planned gifts.

E. Foundation gifts. Different types of foundations are treated differently in regards to the eligibility of their grants as gifts for matching.

Public or private foundations: Grants from foundations such as the Andrew W. Mellon, Rockefeller, and Gladys Krieble Delmas foundations, as well as many others, may count toward match. "Challenge" grants, such as from Kresge or Mellon, may count toward the NEH matching requirement and the NEH funds in turn may count toward the foundation's matching requirement, if the foundation's policies allow. This is called "mirror matching" and is acceptable to NEH. Documentation of the foundation’s permission to allow mirror matching must be provided when the foundation’s grant is certified.

Family foundations or funds: Gifts from a foundation or fund established and managed by a single family for the purpose of making charitable contributions to non-profit entities may count toward match. Gifts from family foundations should be classified as gifts from individuals (that is, listed under category #1 on the certification form).

Institution-specific foundations: Many foundations are created for the purpose of raising money (and, sometimes, managing the endowment) for a single entity, such as a university, a state humanities council, or a museum. Such a foundation may be the challenge grant recipient of record. If the foundation is not the grantee of record, a memorandum of agreement should be provided designating the foundation as agent for the grantee for soliciting and receiving donations for the challenge grant. An institution-specific foundation may not make donations to its own institution's challenge grant. Gifts that meet all eligibility criteria except that they are made to an institution-specific foundation rather than directly to the grantee may be eligible for matching.

Examples:

University X has a challenge grant to endow a computer center for the humanities. The University X Foundation gives $400,000 from its own assets, which are normally used to support various special projects at the university, in response to the challenge grant. This donation cannot count toward match: the foundation is not a disinterested third party, and the gift is too much like a shift of internal assets.

The foundation donates $100,000 that it can identify as coming originally from Donor Z, who gave the funds to the foundation within the fundraising period (five months prior to the application deadline through the end date of the period of performance). If Donor Z signs a letter to the foundation stating that her gift may be used for the challenge grant, this $100,000 may count as a restricted gift. If Donor Z does not sign such a letter, the $100,000 is still eligible, but only as an unrestricted gift.

Community foundations: Foundations established to solicit and manage donations to various charities within a given community may give in response to a challenge grant and have their gifts count toward match (and should be categorized as #3 "foundation" on the certification form). If, however, the community foundation is the challenge grant recipient of record or is designated as the agent of the grantee authorized to solicit and receive gifts on the grantee's behalf, then the community foundation is governed by the rules for institution-specific foundations.

Donations from identifiable gift funds, such as family funds held and managed within the community foundation, can count as match and should be categorized as donations from individuals.

Donor-advised funds: A donor-advised fund is one that has been donated to a charitable entity such as a community foundation or a commercial gift fund. Legally the gift becomes an asset of the receiving foundation and the donor has no final control over how the gift will be used. However, the donor may advise the foundation on uses. If a foundation (such as a community foundation) identifies a gift as based on the advice of a donor, for challenge grant purposes the gift is treated as emanating from the original donor-advisor. Thus, even a community foundation that has been designated the agent for receiving gifts for the challenge grantee may give a donor-advised gift that can count toward match. Donations from donor-advised funds should be categorized as from #1, "individuals." Documentation from the donor-advisor must be provided to NEH with the certification. However, the donor-advisor cannot pledge a gift from the donor-advised fund.

F. Ineligible Gifts. The following are examples of ineligible gifts

- Gifts deferred beyond the end date of the grant period of performance.

- Discounts on goods or services provided through contracts.

IV. Certification of Gifts

Certification is the process by which the recipient certifies to NEH that eligible gifts have been raised to meet the NEH Challenge Grant. Recipients must submit donor documentation with the gift certification for cash gifts from individual donors over $25,000. Supporting documentation for other kinds of gifts must be submitted with the gift certification. The certification and documentation are reviewed by the NEH Office of Grant Management, which will then send acknowledgment and approval via an electronic notice of award that obligates related grant funds. Recipients may then submit payment requests to draw down those funds (see section V. Payment).

A. Record Keeping for Matching Gifts. The recipient must keep on file documentation showing 1) the value and source of all donations; 2) the donor's awareness, in the case of a restricted gift, that it is being used for the approved challenge grant purposes outlined in the proposal; 3) evidence that the gift was received during the fundraising period (five months prior to the application deadline through the end date of the period of performance); and 4) the expenditure of grant and matching gift funds during the period of performance. Documentation for all matching gifts and other evidence of eligibility, such as brochures, posters, recordings, newsletters, and other publicity material, should be maintained by the grant recipient for at least three years after the recipient’s submission of the final Federal Financial Report. Copies of gift documentation must be submitted when the gift is certified. All records are subject to audit. (See 2 CFR §§ 200.333 – 337[vi] for additional information regarding record retention and access.)

- Sample Donor Transmittal Letter. A donor transmittal letter of some type is required for all restricted gifts of $25,000 or more. The following donor transmittal letter is a model that contributors may use:

(Date)

Dear (authorizing official):

In support of your National Endowment for the Humanities challenge grant [or proposal] (#C______________), I/we hereby give the sum of $______________ to be used to match and to be expended for the approved purposes of this grant. Payment in the form of _______________________ is enclosed.

Sincerely,

(Signature),

Name and Address of Donor

- In the case of restricted donations of less than $25,000, it is not necessary to have each donor complete such a letter if the solicitation material includes sufficient information to document that the purpose of the gift is to match the NEH challenge or is specifically given to fund one of the approved purposes of the Challenge Grant.

B. Certification. See the original challenge grant offer letter for annual deadlines for certifying matching funds. Grant recipients are encouraged to certify matching funds at any time during the year to release all or part of that year's federal funds or simply to fulfill any portion of the matching requirement. Any matching funds certified in excess of one year's requirement will be credited toward the requirements for subsequent years and may sometimes be used to release federal funds ahead of schedule. Recipients should not certify more often than monthly and should not certify less than $5,000.

- What to Report. The certification form (PDF) found in Appendix 1 is used to report the eligible matching gifts grouped according to the appropriate donor categories (described in the next subsection). The certification form sets forth in three columns 1) the amounts, if any, of gifts previously certified and the date of the last certification; 2) the amounts of new gifts (and pledges) currently being certified; and, by adding the first two columns together, 3) the current cumulative total of gifts raised (including pledges to be fulfilled) within the fundraising period (five months prior to the application deadline through the end date of the period of performance).

- The certification form and copies of solicitation materials (where appropriate) are the only documents necessary to certify most gifts or pledges of cash under $25,000. Gifts over $25,000 require a transmittal letter. However, certain types of gifts—real estate, in-kind donations, special appropriations, planned gifts, gifts from estates, alternate arrangements—require additional documentation. See Section IV. C.

- The certification form must be completed and submitted electronically via eGMS Reach, NEH’s online grant management system located at https://securegrants.neh.gov/eGMS-Reach/Login.aspx.

- Donor Categories on the Certification Form. The categories relate to the donor source and do not specify the form of the gift.

- Individuals. Individual persons not included in category six (affiliated groups), but including family foundations and donor-advised funds.

- Corporations and businesses. Businesses, corporations, and corporate or company-sponsored foundations. Many businesses sponsor a program whereby an individual employee's gift to a cultural organization may be complemented by an additional amount from the employer. The company's gift is responsive to the initiative of the employee and can count for matching purposes. The sum of the employee's gift plus the match from the employing company should be included under category number one for gifts from individuals.

- Private or public foundations. See section III. E. Family foundations and donor-advised funds should be categorized as individual donations (category #1).

- Labor unions or professional or trade associations.

- Nonfederal government units, such as state legislative bodies or agencies, county boards, or municipal sources.

- Affiliated groups. Pooled rather than individual sources or other separate but associated groups. Examples include alumni associations, the class of 1963 as a group, or "friends" groups.

- Special events and benefits. Events such as auctions, raffles, benefit concerts, or other special fundraising events.

- Other. Miscellaneous sources not classified above. If the gifts listed under this category amount to more than 10 percent of the matching requirement, please describe the donor sources in an accompanying narrative.

Questions about determining the appropriate category of a gift should be directed to the NEH Office of Grant Management or the Office of Challenge Grants.

- Pledges included in certification. As indicated in Section III.C., pledges made in response to the challenge grant may be eligible as long as they are paid by the end of the period of performance. If any pledge donor defaults in payment, then the grant recipient must either 1) enforce collection of the pledge within the period of performance, 2) substitute and report to NEH other eligible gifts, or 3) return to NEH that portion of federal funds left unmatched because of the defaulted pledge or pledges. Concerns about defaulting should be discussed with Endowment staff at the earliest possible time. With the submission of the final certification, the grant recipient must attest that all certified pledges have been paid. It is important that the grant recipient keep clear records of all payments received against eligible certified pledges to prevent duplication of those amounts in subsequent certifications.

In the case of pledges for a restricted gift of less than $25,000, it is not necessary to have each donor complete a separate letter if there is some other form of making a written pledge available through the solicitation material. For example, documentation could be in the form of a pledge card signed by the donor that contains a preprinted reference to the use of the donation to match the NEH challenge and shows the donor's address, the eligible amount of the gift, and the date by which the gift has been or will be paid (within the fundraising period). Pledges of unrestricted gifts require no reference to the NEH challenge, except that the gifts must be pledged and paid within the fundraising period.

- Sample Pledge Letter. All pledges must be in writing. The following sample letter may be used and adapted to particular circumstances:

Dear (authorizing official):

In support of your National Endowment for the Humanities challenge grant [or proposal] (#CHA_____________), I/we hereby pledge the sum of $_______________ to be used to match and to be expended for the approved purposes of this grant. I/we will make payment on this gift directly to (name of grant recipient organization) on or before (date of payment), but in no event later than (end date of the period of performance).

Sincerely,

(Signature),

Name and Address of Donor

The reference to the challenge grant or its purpose is required for pledges of restricted gifts but is not necessary for pledges of unrestricted gifts.

C. Additional Documentation. Certain gifts require additional documentation to supplement the certification form and transmittal letters. (Please note that the certification form should include the total of all gifts.)

- Gifts of real estate—restricted:

-- a signed and dated copy of the donor's gift transmittal letter indicating whether the property will produce income or is to be liquidated in order to achieve the purpose of the grant; and

-- if the gift is converted into cash by means of sale, a copy of the bill of sale (indicating the net sale value).

- Gifts of real estate—unrestricted:

-- documentation indicating whether the property will produce income or is to be liquidated;

-- if the gift is converted into cash by means of a sale, a copy of the bill of sale (indicating the net sale value); and

-- documentation indicating the date of the gift.

- In-kind gifts of services, materials, or other types of third-party, non-cash tangible donations, which may count only as restricted gifts, not as unrestricted gifts:

-- regardless of the gift's fair-market value, a signed and dated transmittal letter from the donor;

-- documentation of the date of the gift;

-- a description of the objects, materials, or services provided and their fair-market value; and

-- for a gift of service, the total number of hours contributed and an explanation of the fair-market value of the labor computed on an hourly basis.

- Special Appropriations: a copy of the appropriating legislation that indicates the date of the appropriation and that designates the funds specifically for the challenge grant or its purposes. (If another form of documentation is proposed, please consult with NEH staff.)

- Planned Gifts and Gifts from an Estate: See Section III.D. for the documentation required for certification of a planned gift or a gift from an estate.

- Alternate Arrangements: Any arrangement to allow an entity other than the grant recipient to receive matching gifts on the grantee's behalf, or to hold or manage the challenge grant funds, either federal or nonfederal, must be approved by NEH (see III.A.5.). The documentation that will be required depends on the particular circumstances; please consult with NEH staff.

- Unrestricted Gifts: When certifying unrestricted gifts, grantees must document the nature of any fund that, by whatever name, contains gifts that are considered to be unrestricted and transferred to the challenge grant. The fund must be explained. The grant recipient must also provide documentation as to the date the gift was given.

V. Payment

Payment for approved direct expenditures (capital expenditures, sharing of collections, purchase of equipment and software, and fundraising costs) should be requested in accordance with the payment procedures found in section 4 of the General Terms and Conditions for Awards to Organizations (for grants and cooperative agreements issued December 26, 2014 or later).

Payment for deposits into a short term endowment (or spend-down) funds can be requested immediately upon notification from the NEH that match certification has been approved and related funds for this purpose have been obligated. Funds earmarked for short term endowment (or spend-down) funds are considered to be “expended” upon deposit into an income-earning account established as an endowment fund.

VI. Failure to Meet Required Match

A. Forfeiture. If sufficient donations are not raised in any given year of the period of performance, the federal offer for that year may have to be forfeited. The forfeiture of some or all federal funds in any given year proportionately reduces the total matching requirement.

B. Refunds. Failure to complete matching requirements in the final grant year would require the return of some federal funds.

C. Extensions. A request to extend the deadline for certification of required matching funds should be made at least one month prior to the deadline. All extensions are at the discretion of the Endowment. Extensions that would defer an offer of federal funds from one fiscal year to a later fiscal year can be granted only if NEH budget and program constraints permit.

VII. Reporting Requirements

A listing of the required reports and the reporting due dates will be provided following the receipt of the first certification of gifts. All reports must be submitted electronically via eGMS Reach, NEH’s online grant management system located at https://securegrants.neh.gov/eGMS-Reach/Login.aspx.

A. Annual Certifications. The Endowment requires recipients to certify matching funds at least annually (and as frequently as monthly).

The form entitled Certification of Matching Gifts for NEH Challenge Grants[vii] (PDF) is available on the NEH website and is also contained in eGMS Reach.

B. Interim Performance Reports. These reports will usually be written by the project director and should be submitted with the gift certification on or before the certification deadline. The reports should include:

- A statement summarizing the approved plan of expenditures and enumerating the disposition (pledged, invested, or expended) of both federal and nonfederal funds for each purpose thus far. If funds are being used to create an endowment, an explanation of how the yield is being put to use should be added. Where such revenues are already supporting expenditures (for example, new positions), the activities supported should be described in detail. For instance, when an endowed position is filled, the incumbent's résumé should be attached to the report;

- The effects of the grant expenditures (if any) thus far on humanities programs or activities. Any changes in the status of humanities programs or activities since the proposal was written or since the last report was submitted should be discussed;

- If applicable, any unexpected impact—positive or negative—resulting from the challenge grant;

- The progress of the fundraising plan, including successes, problems, and variety of fundraising techniques employed. Please append to the narrative report samples of brochures, mailings, and publicity regarding the fundraising efforts;

- A description of the ways in which NEH support has been and will continue to be acknowledged (see Section IX, "Acknowledgement Guidelines")/

C. Final Performance Report (and Certification). The final narrative report should be submitted within 120 days if you received your award on or after November 12th, 2020. If you received your award before November 12th, 2020 your final report is due within 90 days of the end of your period of performance.

The final performance report should include:

- A summary of the total grant fundraising (both federal and nonfederal) and of the expenditures for each purpose.

- An assessment of the success of the fundraising campaign. Describe especially effective (or ineffective) strategies, and discuss the leveraging effect of the NEH challenge.

- An assessment of the degree to which the challenge grant has met the goals set forth in the original application. Discuss the overall impact of the grant on the institution's humanities activities and finances.

- A description of how the challenge grant has enhanced awareness of the humanities, both internally and for the general public. Please provide examples. Upload samples as well as information on the products produced under the grant to the eGMS Reach Products and Prizes tab.

- A description of how NEH support has been acknowledged for endowment and collection sharing projects; and how NEH support will continue to be acknowledged for construction projects (see Section VIII, "Acknowledgement Guidelines").

The final performance report should include a final certification form that shows that all pledges used to match the grant have been collected or that other eligible matching gifts have been substituted for uncollected pledges. Please complete the line on the certification form acknowledging this condition.

An institution may submit a final performance report at any time after receiving all federal funds that are due and certifying completion of its matching requirement.

D. Follow-up Reports: While NEH requires no formal reports after the close of the challenge grant, grantees are strongly encouraged to send information on the continued progress of the activities and programs supported by the grant to the Office of Challenge Grants. NEH may on occasion survey grant recipients about the results of their challenge grants.

E. Final Federal Financial Report (FFR) SF-425[viii]: A final Federal Financial Report (FFR) SF-425 will be due within 120 days if you received your award on or after November 12th, 2020. If you received your award before November 12th, 2020 your final report is due within 90 days of the end of your period of performance. For further details, please see the Payment Requests and Financial Reporting Requirements[ix].

F. Extensions of Reporting Deadlines: A grant recipient may request an extension for the submission of reports. In all cases, requests for extensions should be made via eGMS Reach at least thirty days before the reporting deadline.

VII. Acknowledgment Guidelines

Because donors of restricted gifts must be aware that their gifts are to be used to match the NEH challenge, all solicitations during the campaign for challenge grant donations must refer explicitly and prominently to NEH and to the humanities.

Equally important, beyond the fundraising campaign, is acknowledgment of NEH support. Please see item 3. Acknowledgment of Support and Disclaimer in the General Terms and Conditions[x] for additional information. Also note the following:

- Buildings or sites constructed or renovated with NEH support should include a prominently displayed plaque or other permanent sign acknowledging support from the NEH. The NEH should be included in any list of donors in reports about fundraising campaigns of which the challenge grant was a part.

- When appropriate, the term "humanities" should be included in the name of galleries, classrooms, library rooms, and other named entities supported by the challenge grant. You are urged to consult with staff in the Office of Challenge Grants about whether to include NEH designation in a name or title.

- Grant recipients are urged to find other ways to acknowledge NEH support and, as importantly, bring the achievements of the humanities to public attention. Grantees are also urged to bring to the Endowment's attention information about openings, news conferences, celebrations, or other events deriving from challenge grant support.

Appendices

Appendix 1

The form entitled Certification of Matching Gifts for NEH Challenge Grants (PDF) is available on the NEH website and is also contained in eGMS Reach.

Appendix 2

Special requirements for projects involving construction, renovation, repair, rehabilitation, and ground and visual disturbances

All NEH-funded projects involving construction, renovation, repair, rehabilitation, or ground or visual disturbances must comply with all applicable federal laws including those addressing wage rates, disability rights, historic preservation and environmental policy. Applicants are expected to familiarize themselves with the Davis-Bacon Act[xi] (40 U.S.C. §276a through 276a-5), the Americans with Disabilities Act of 1990[xii] (42 U.S.C. §§ 12101-12213), and Section 106 of the National Historic Preservation Act[xiii] (54 U.S.C. §306108) and its implementing regulations (36 C.F.R. Part 800), and the National Environmental Policy Act (NEPA), as amended, 42 U.S.C. §4331 et seq.

I. Davis-Bacon Act

Be advised that any construction or renovation contracts in excess of $2,000 awarded by recipients or subrecipients and funded by federal funds, in whole or in part, are subject in their entirety to the Davis-Bacon Act as amended, (40 U.S.C. §276a through 276a-5) as supplemented by Department of Labor regulations (29 CFR Part 5, “Labor Standards Provisions Applicable to Contracts Covering Federally Financed and Assisted Construction”). Grant recipients are required by law to furnish assurances to the Secretary of Labor that all laborers and mechanics employed by contractors or subcontractors on Endowment-supported construction projects shall be paid wages at rates that are not less than those prevailing on similar construction in the locality, as determined by the Secretary of Labor. In addition, contractors must be required to pay wages not less than once a week. See 2 CFR 200 Appendix II – Contract Provisions for Non-Federal Entity Contracts Under Federal Awards[xiv] for additional information.

Additional information is available by contacting the U.S. Department of Labor, Wage and Hours Division, Division of Contract Standards and Operations, 200 Constitution Avenue, NW, Washington, D.C., 20210; 1 (866) 487-2365 or 1 (202) 693-0087.

II. Americans with Disabilities Act:

Article 26 (e) of NEH’s General Terms and Conditions for Awards[xv] requires grant recipients and subrecipients to adhere to the Americans with Disabilities Act (ADA). Title III of the ADA covers places of public accommodation (such as museums, libraries and educational institutions) and includes a specific section regarding new construction and alterations in public accommodations.

The website www.ada.gov[xvi] provides comprehensive information that the grantee can consult concerning compliance with the ADA, including the text of the legislation, the revised regulations implementing Title II and Title III of the ADA, and the 2010 ADA Standards for Accessible Design.

III. Section 106 of the NHPA:

Prior to the expenditure of any federal funds, Section 106 requires NEH to review the effects of projects offered NEH funding on historic properties that are listed or eligible for listing in the National Register of Historic Places. When applicable, NEH must also provide the Advisory Council on Historic Preservation (ACHP) an opportunity to comment on such projects prior to the expenditure of any federal funds.

To understand and navigate the Section 106 review process, recipients should familiarize themselves with the Section 106 materials available here[xvii]. There is no formula for how long a given Section 106 review may take, so recipients should build sufficient time into their project plans to allow for a potentially lengthy review. NEH does not formally initiate a Section 106 review until it offers support for a project. A recipient offered a challenge grant cannot begin any work involving construction, renovation, repair, rehabilitation, or ground or visual disturbances—and that NEH cannot release any federal funds—until NEH concludes its Section 106 review.

IV. Environmental National Policy Requirements

In accordance with the National Environmental Policy Act[xviii] (NEPA, at 42 U.S.C. §4321, et seq.), successful challenge grant applicants engaging in construction and major alterations and renovations must identify the impact the project may have on the quality of the human environment and assist the NEH to comply with NEPA and to prepare Environmental Impact Statements or other required environmental documentation. In such cases, the recipient agrees to take no action that will have an adverse environmental impact (for example, physical disturbance of a site such as breaking of ground) until the agency provides written notification of compliance with the environmental impact analysis process.

Also see article 26 (e) of NEH’s General Terms and Conditions for Awards[xix] for additional environment requirements that grant recipients and subrecipients must adhere to.

Appendix 3

Federal Interest in Real Property

Real property is land, including land improvements, and buildings; it excludes moveable machinery and equipment. The title to real property acquired or improved under an NEH award vests with the recipient. (See 2 CFR §200.311 Real property.)

However, when a recipient uses NEH funds to purchase land or buildings or to construct or renovate a facility, it creates a “federal interest.” Federal interest is a property right which secures the right of the federal awarding agency (NEH) to recover its percentage of funding for the purchase of land or buildings, or for substantial improvements to a facility (construction or major renovations), in the event the property is no longer used for humanities purposes by the recipient or upon the disposition of the property. The Federal Government’s interest is intended to protect the purpose for which the federal funds were originally awarded.

Period of Federal Interest

When NEH funds are used to purchase, construct and/or renovate real property, the period of federal interest extends five (5) years from the period of performance end date. During this time, the real property must be used for the intended humanities purpose, the owner may not sell, lease, transfer, assign, mortgage, or otherwise convey any interest in the property without prior written approval from the NEH Office of Grant Management. In the event the property is no longer used for humanities purposes by the recipient or upon the disposition of the property during the period of federal interest, the recipient must submit a prior approval request and the SF-429C Real Property Status Report Attachment C (Disposition or Encumbrance Request) through eGMS Reach.

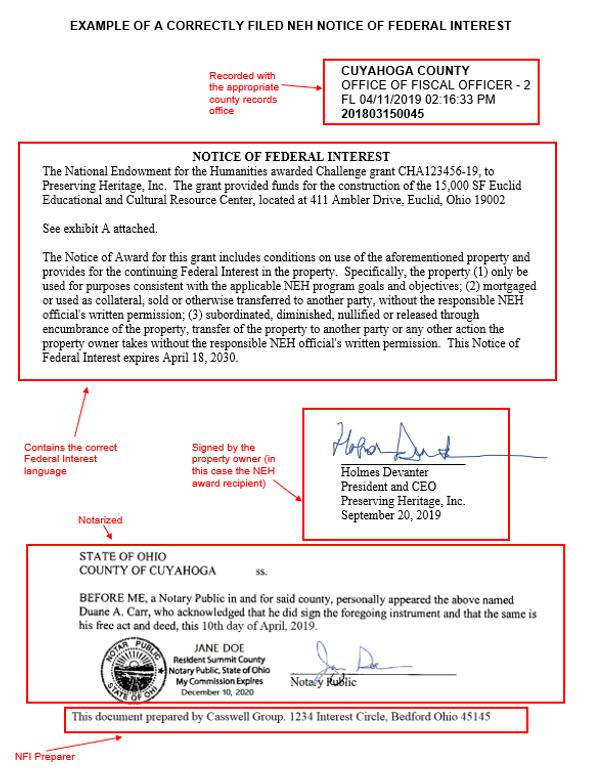

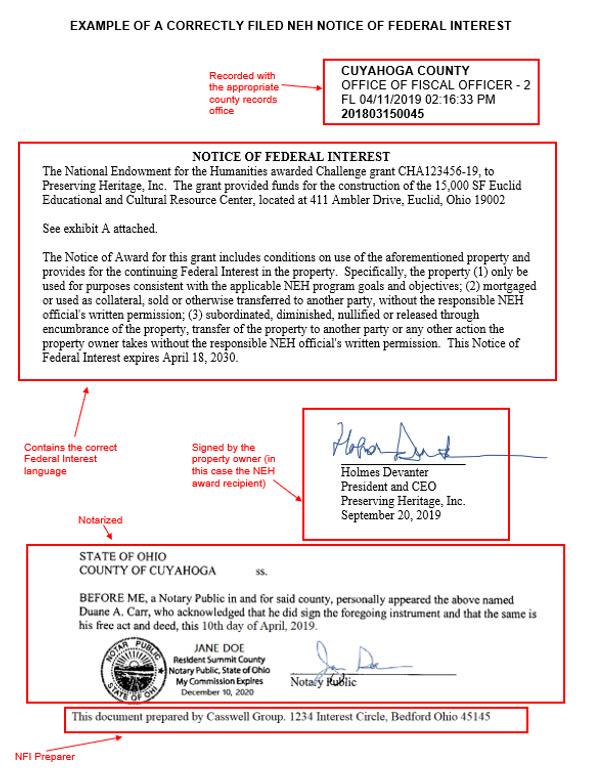

Notice of Federal Interest

When the NEH provides funding greater than $500,000 for the purchase of land or buildings, or for new construction, expansion or major renovations, the property owner may be required to attach a lien to the property called a Notice of Federal Interest (NFI) (see 2 CFR §200.316 Property Trust Relationship).

The property owner must record an NFI in the official real property records for the jurisdiction where the property is or will be located. The NFI must be recorded before construction with NEH funds begins and before NEH funds may be drawn down. The NFI will expire five (5) years, from the NEH award period of performance end date. Once the NFI expiration date has passed, no further action is necessary to release the federal interest in the real property.

Annual Reporting

Recipients using NEH funds to purchase land or buildings, or for new construction, expansion or major renovations must submit the SF-429A Real Property Status Report (General Reporting) annually during the period of performance and the five-year period covered by the NFI.

Frequently Asked Questions

Q1: Does federal interest in real property purchased, constructed or improved with NEH funds exist if a recipient is not required to file a Notice of Federal Interest (NFI)?

A1: Yes. For real property projects funded by the NEH at $500,000 or less, which do not require an NFI, federal interest still exists for a period of five (5) years from the period of performance end date. Recipients must still maintain adequate documentation regarding protection of federal interest. If the building is leased, this includes, but is not limited to: written communications with a lessor related to protecting such interest during the lease period, in accordance with the standard award terms and conditions. The NEH, the NEH Inspector General, the Government Accountability Office, or any of their authorized representatives must be given access to these documents upon request (see 2 CFR §200.336 Access to records).

Q2: Does NEH take a subordinate position to pre-existing mortgage holders and lenders on potential debt financing for projects?

A2: Yes. NEH's NFI is subordinate to all pre-existing mortgages or obligations recorded against the property. This includes loans and obligations identified by the recipient as sources of financing for the NEH project that are recorded prior to filing the NFI. Pursuant to the NFI, future modifications to existing mortgages, new mortgages, and related types of financing, will require NEH review and prior approval, through eGMS Reach.

Q3: The NEH award required that the facility owner file a Notice of Federal Interest (NFI) against a facility deed. What if the owner wants to secure additional mortgages, lease the facility to an entity that does not provide humanities programming, or sell the facility?

A3: Activities such as new mortgages, selling the facility, or leasing the facility to an entity that does not intend to use it for humanities-related purposes during the period of performance and the five (5) years following the end date, requires prior approval from NEH. The recipient must submit a prior approval request and the SF-429C Real Property Status Report Attachment C (Disposition or Encumbrance Request) through eGMS Reach.

Reviewing federal interest requests takes time and NEH requests patience and cooperation in the process. If the recipient provides detailed requests and supporting documentation up front, this will aid NEH in expediting reviews.

Q4: Are there additional requirements for leased property?

A4: Yes. If an organization applies to NEH to renovate leased property, it must submit a copy of the existing or proposed long-term lease agreement (the lease must extend at least five (5) years from the end of the proposed period of performance), the landlord or lessor’s consent to the renovation, and the landlord or lessor’s agreement to file an NFI (as applicable). The NFI requirements listed above apply to leased property.

Q5: How long does NEH’s federal interest in real property last?

A5: NEH’s federal interest will expire five (5) years after the period of performance end date.

Q6: How do I file a Notice of Federal Interest (NFI)?

A6: The process to record an NFI for an NEH-funded project is as follows:

General

- Within the United States, except Hawaii, the NFI must be filed in the county or district office in which the facility is located. Often this is the County Court Clerk, Probate Office or the Register of Deeds. In the State of Hawaii, the NFI must be filed with the State Department of Land and Natural Resources, Bureau of Conveyances.

- Please understand that local governments may have different formatting requirements. It is important to check with the office before filing, as it may eliminate unnecessary trips.

- The county government will provide a copy of the recorded NFI with the county stamp, with a date, and either receipt information, or the final reference number (book and page, file, etc.).

NFI Document must include:

- The property owners correct legal name and current mailing address.

- The NEH federal award identification number (grant number).

- The description of the project, which should clearly describe the new construction project, purchase of land or buildings, or alteration and renovation.

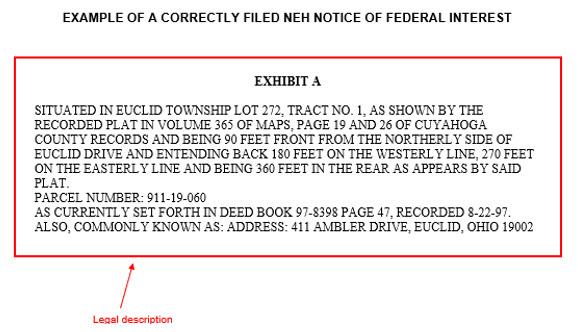

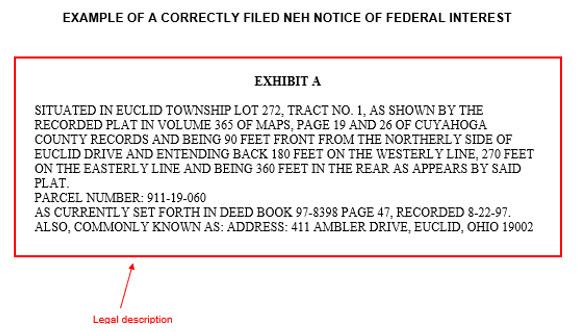

- The full legal description of the property in the deed. However, Township and Range, or Map, Block, and Lot number will be accepted. A physical address may be included, but does not constitute a legal description in itself.

- A statement that the real property: (1) will only be used for purposes consistent with the applicable NEH program goals and objectives; (2) will not be mortgaged or used as collateral, sold or otherwise transferred to another party, without the NEH Office of Grant Management's written permission, and; (3) the federal interest cannot be subordinated, diminished, nullified or released through encumbrance of the property, transfer of the property to another party or any other action the property owner takes prior to the expiration date of the NEH NFI without the NEH Office of Grant Management's written permission.

- The expiration date of the NEH NFI will be five (5) years after the period of performance end date.

- The name and title of the person or company who drafted the notice.

- The signatory of the NFI should be the owner of the property. This indicates the owner’s consent to have a lien filed on the property.

Review, Sign, Notarize, and File

- The draft NFI must be submitted to the NEH for review and approval of the restrictive language and expiration date.

- The NFI must then be notarized and embossed with a notary seal. The NFI must then be recorded with the county government.

- A copy of the recorded NFI must be submitted to the NEH.

Q7: Does NEH require a copy of the Notice of Federal Interest (NFI)?

A7: Yes. A copy of the recorded NFI must be submitted to the NEH through eGMS Reach.

Q8: What reporting requirements apply during the period covered by the Notice of Federal Interest (NFI)?

A8: The recipient must submit the SF-429A Real Property Status Report (General Reporting) annually during the period of performance and the five-year period covered by the NFI.

Source URL: https://www.neh.gov/grants/manage/administration-neh-challenge-grants

Links:

[i] https://www.ecfr.gov/cgi-bin/text-idx?SID=1c7d9eab08a2575785c5f4e3154da42c&mc=true&node=pt2.1.200&rgn=div5#_top

[ii] https://www.neh.gov/grants/manage/general-terms-and-conditions-awards-organizations-grants-and-cooperative-agreements-issued-december

[iii] https://securegrants.neh.gov/eGMS-Reach/Login.aspx

[iv] https://www.ecfr.gov/cgi-bin/text-idx?SID=1c7d9eab08a2575785c5f4e3154da42c&mc=true&node=pt2.1.200&rgn=div5#sp2.1.200.e

[v] https://www.ecfr.gov/cgi-bin/text-idx?SID=1c7d9eab08a2575785c5f4e3154da42c&mc=true&node=pt2.1.200&rgn=div5#se2.1.200_1306

[vi] https://www.ecfr.gov/cgi-bin/text-idx?SID=1c7d9eab08a2575785c5f4e3154da42c&mc=true&node=pt2.1.200&rgn=div5#sg2.1.200_1332.sg6

[vii] https://www.neh.gov/files/grants/challengegrantcertification2018.pdf

[viii] https://www.gsa.gov/forms-library/federal-financial-report

[x] https://www.neh.gov/grants/manage/general-terms-and-conditions-awards-organizations-grants-and-cooperative-agreements-issued-december#acknowledgment

[xi] https://www.dol.gov/oasam/regs/statutes/276a.htm

[xii] https://www.ada.gov/pubs/ada.htm

[xiii] https://www.neh.gov/grants/manage/section-106-the-national-historic-preservation-act

[xiv] https://www.ecfr.gov/cgi-bin/text-idx?SID=1c7d9eab08a2575785c5f4e3154da42c&mc=true&node=pt2.1.200&rgn=div5#ap2.1.200_1521.ii

[xv] https://www.neh.gov/grants/manage/general-terms-and-conditions-awards-organizations-grants-and-cooperative-agreements-issued-december#nondiscrimination

[xvi] https://www.neh.gov/grants/manage/general-terms-and-conditions-awards-organizations-grants-and-cooperative-agreements-issued-december#nondiscrimination

[xvii] https://www.neh.gov/grants/manage/section-106-the-national-historic-preservation-act

[xviii] https://ceq.doe.gov/laws-regulations/laws.html

[xix] https://www.neh.gov/grants/manage/general-terms-and-conditions-awards-organizations-grants-and-cooperative-agreements-issued-december#nondiscrimination